When you hear deductible, the amount you pay for covered health services before your insurance plan starts to pay. It's not just a number on a paper—it's the gatekeeper between you and your meds. Also known as an out-of-pocket threshold, your deductible determines whether you pay full price for your prescriptions or start getting discounts from your plan. If you haven’t met it this year, your insulin, blood pressure pills, or asthma inhaler could cost you $100, $200, or more per refill. That’s not a typo. That’s how the system works.

Most people think insurance means lower costs right away. But that’s only true after you hit your deductible. Until then, you’re on your own. And if you’re on chronic meds, that adds up fast. A $1,500 deductible means you pay the first $1,500 of your medical bills—including prescriptions—before your plan kicks in. That’s why so many people skip refills, split pills, or turn to Canadian pharmacies for cheaper options. It’s not reckless. It’s rational.

Your deductible doesn’t just affect prescriptions. It ties into your overall health spending. If you have a high-deductible plan, you might also have an HSA, which lets you save pre-tax money for meds. But not everyone knows how to use it right. Some people fund it and then forget about it. Others don’t realize they can use HSA funds for over-the-counter meds without a prescription anymore. And if you’re on multiple drugs, your deductible resets every year—so if you met it last December, you’re back to square one in January.

Here’s the thing: not all plans are created equal. A $500 deductible with a $20 copay for generics might be better than a $3,000 deductible with a $10 copay. You need to look at the whole picture. And if you’re on expensive brand-name drugs, your deductible might be the biggest barrier you face—not the price tag itself. That’s why talking to your doctor about staying on brand, or switching to a generic that actually works for you, isn’t just a conversation—it’s a cost-saving move.

And it’s not just about insurance. Some pharmacies offer discount programs that stack with your deductible. Others let you pay cash and still get lower prices than your insurance copay. That’s why checking prices at Canadian pharmacies isn’t just for people without insurance—it’s for anyone who’s tired of paying full price before their deductible kicks in.

There’s no magic fix. But understanding your deductible gives you power. You can plan your meds around it. You can time your refills. You can compare prices before you fill. You can ask your doctor if a cheaper alternative exists. And you can decide whether to stick with your current plan or switch next year.

Below, you’ll find real stories and practical guides on how people manage their meds under high deductibles. You’ll see how some avoid price spikes by switching to generics, how others use patient assistance programs, and how a few even found better deals by ordering from Canada. These aren’t theoretical tips. They’re what people actually do when their insurance doesn’t cover what they need.

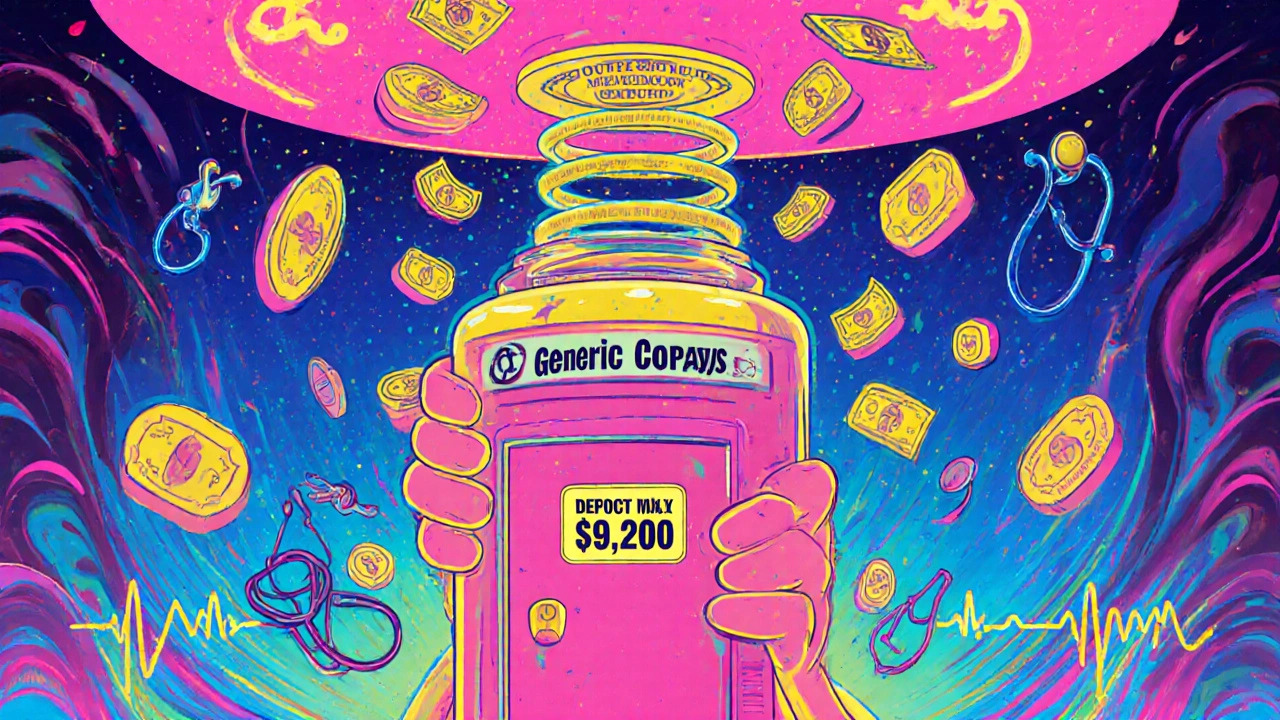

Generic prescription copays count toward your out-of-pocket maximum but usually not your deductible. Learn how this works, why it causes confusion, and how to track your costs correctly to avoid unexpected bills.